Assalamualaikum,

Ramai antara kita kini berasa sudah sangat selesa hidup di dalam COMFORT ZONE. Sudah berasa cukup dengan sekadar apa yang ada. Sememangnya kita perlu bersyukur kepada Allah atas atas segala rezeki & nikmat yang diberi.

TETAPI, ada juga SESETENGAH orang yang kononnya sudah 'selesalah sangat' berada di dalam comfort zone ini, sering MENGELUH.

Contohnya salahkan peniaga sebab naikkan harga barang, salahkan boss sebab tak naikkan gaji, salahkan company sebab tak bagi bonus, salahkan sekolah/kolej/university sebab naikkan yuran pelajaran, salahkan hospital sebab charge hospital mahal sangat, dan bermacam-macam lagi kesalahan orang lain.

Mereka sahajalah yang tak bersalah dan menjadi mangsa keadaan.

Jadi ada antara mereka yang memberi ALASAN tak boleh nak spend untuk bersedekah, menderma, berwakaf, sebab duit utk hidup diri sendiri & family pun cukup-cukup makan aje.

Nak beli buku tambahan/tuition untuk pelajaran anak pun tak boleh. Nak hantar service maintenance kereta pun bertangguh-tangguh, sampai last-last kereta tu sendiri dah rosak teruk, dan lagi banyak nak kena repair. Semuanya sebab nak cut expenses.

Nak buat macam mana, dah rutin kerja kita PERGI PAGI, BALIK PETANG. DAPAT GAJI BAYAR HUTANG. Produktif atau tidak produktif kita di tempat kerja, akhir bulan tetap akan mendapat jumlah gaji yang sama...tetapi HUTANG & KOMITMEN semakin bertambah. Selesa sangat kah kita hidup macam tu?

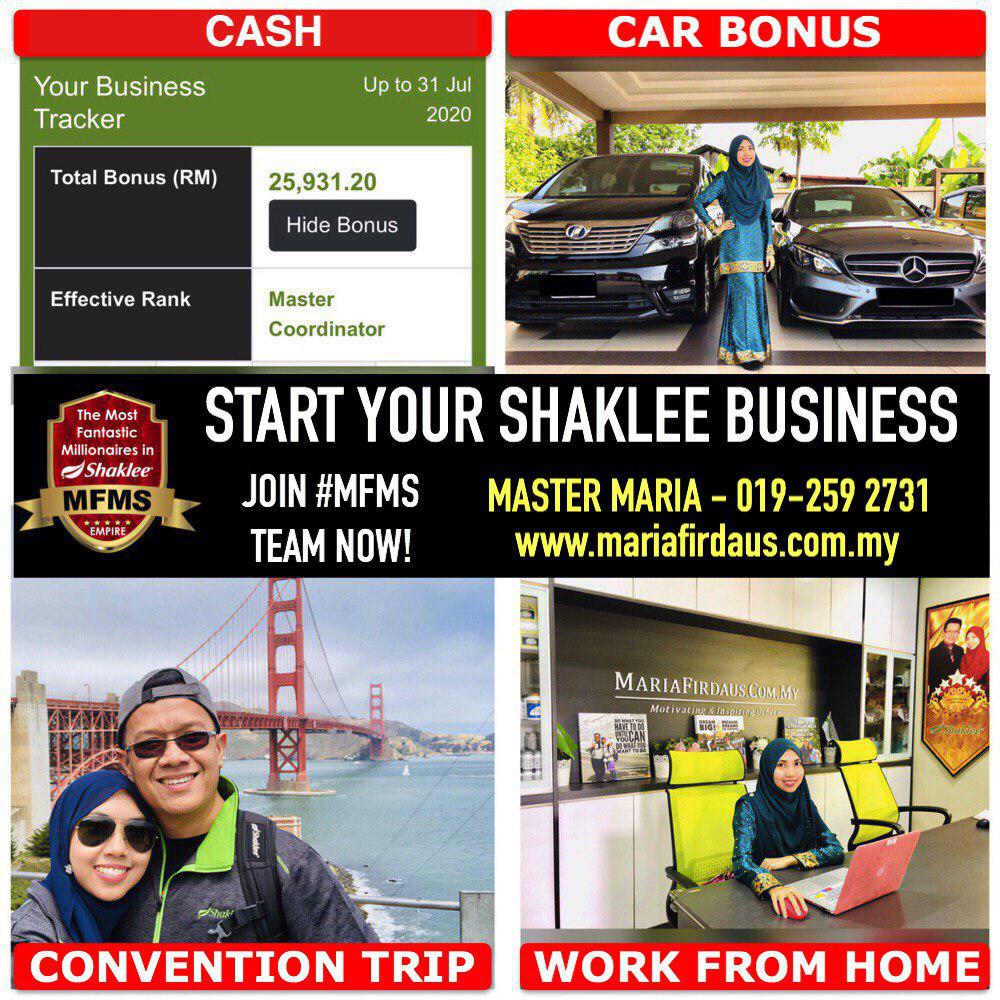

Maria dulu pun sebenarnya tergolong dalam kumpulan yang suka MENGELUH ni. Tapi kini Alhamdulillah, Allah sudah sedarkan Maria tentang keburukan sifat MENGELUH ini. Kini Maria sedang berusaha untuk ke arah mencapai Financial Freedom dengan menjalankan perniagaan. Maria yakin yang 9/10 pintu rezeki adalah melalui perniagaan. Semoga Allah permudahkan.

This is a very nice article from Robert Kiyosaki, the writer of RICH DAD, POOR DAD book, on the FINANCIAL INTELLIGENCE.

Semoga ianya dapat mengubah mindset kita, supaya jangan hanya tahu BERJIMAT sahaja. Tetapi kita juga perlu tahu saluran yang terbaik untuk SPEND harta kita, agar rezeki yang Allah beri dapat DIGANDAKAN dan beri lebih manfaat kepada diri, keluarga, masyarakat dan ke arah menegakkan Islam.

ERTI HIDUP PADA MEMBERI (Pinjam ayat dari SaifulIslam.com). Selamat Membaca! :)

------------------------------------------------------------------------------------------

Don't Cut Expenses, SPEND! SPEND! SPEND! (Robert Kiyosaki)

If I hear one more financial advisor tell their audience to “cut your expenses,” I may just do something I will later regret. Personally, it’s insulting to me, and it should be to you too, if a financial “expert” thinks we are so unconscious and ignorant that the only way we could possibly reach financial security was by cutting back, reduce what we spend and live a life less than what we really want.

That is LAZY advice. It’s safe advice for the so-called “advisor” because it sounds logical and it won’t cause any flack for the advisor. It’s lazy because the advisor doesn’t have to think.

Cut vs. Spend

Not only is “cut your expenses” lazy advice it is also incorrect advice if you truly want financial security for life. Consider this; you own a duplex that you rent out to two families. In any rental property, as in any business, your three key financial components are: 1) Income 2) Expenses 3) Debt. What are the first questions you should ask when it comes to income, expenses and debt?

INCOME – Very simply, “How do I increase my income?” Whether it’s your rental property, your business, or your personal household, often times, the solution to a financial problem is to increase your income. In real estate, ways to accomplish this is by lowering your vacancies, introduce alternate streams of income such as laundry, and increasing rents.

EXPENSES – Most people automatically ask, “How do I cut my expenses?” Wrong question. The better question to ask is, “How do I spend my money more effectively to increase the value of my property?” “How do I spend my money more effectively to increase the value of my business?” (And yes, this is the question to ask when it comes to you personal finances as well.)

For example, you decide the water bill of the rental duplex you own is too high so you choose to cut that expense by cutting back on the amount of water you use on the property. As a result of the water cutback, your trees and shrubs start dying. Now your tenants are unhappy because the landscape is brown and ugly.

Instead of cutting expenses, the better idea can be to spend money. As with a property I owned, instead of cutting back, I spent more money on additional trees and shrubs. This expenditure increased the curb appeal and made the property more attractive to the residents and prospective tenants.

Because this property now had such a lush look and feel, more and more people wanted to live there. This allowed me to increase the rents. Increased rents equals increased value of the property.

How do you spend money more effectively to increase the value or income, is the exact same question you should be asking of your personal finances. “How can I spend, or use, my money to make more money?”

This is what I mean when I say don’t live below your means, instead expand your means.

Instead of focusing on reducing your expenses, focus instead on INCREASING YOUR INCOME. Increasing your income - not by you working harder, but by spending money that then works hard for you. It takes no brains to cut expenses. Anyone can do that.

It takes CREATIVITY and a little bit of GUTS to figure out how to spend your money to make money. That’s FINANCIAL INTELLIGENCE.

That leaves us with the DEBT question.

The question to ask is, “How do I get the best financing terms?” Too many people focus on the price of the investment, when the deal may be found in the terms, such as the interest rate, length of the loan, interest-only versus 30-year fixed, recourse versus non-recourse. (BTW, if you don’t know the definitions of any of those words, just look them up.)

More than once, I have paid full price in exchange for terms that allowed me to get more cash flow, more time if repairs were needed, or more flexibility for future usage of the property. It’s the financing terms more than the price that can make or break a deal. The beauty of debt (good debt) today is that it is cheap. The interest rate of my first rental property in 1989 was 18%. And we still made it cash flow.

What’s the difference between good debt and bad debt?

Good debt is debt you use to buy assets with. (Assets are things that put money in your pocket whether you work or not.)

Bad debt is debt you use to buy liabilities. (Liabilities are things that take money from your pocket.)

IT’S TIME TO SPEND MONEY!

So,the real key to happiness? The key to having a secure and financially-healthy life is to Spend! Spend! Spend! Just be sure to spend your money in the right places. Financial intelligence is knowing how to spend your money to acquire assets that make money for you versus spending money to acquire liabilities that take money from you. That’s the difference that every Rich Woman knows.

How are you going to spend your money on assets?

Article taken from Richdad.com website.

Ramai antara kita kini berasa sudah sangat selesa hidup di dalam COMFORT ZONE. Sudah berasa cukup dengan sekadar apa yang ada. Sememangnya kita perlu bersyukur kepada Allah atas atas segala rezeki & nikmat yang diberi.

TETAPI, ada juga SESETENGAH orang yang kononnya sudah 'selesalah sangat' berada di dalam comfort zone ini, sering MENGELUH.

Contohnya salahkan peniaga sebab naikkan harga barang, salahkan boss sebab tak naikkan gaji, salahkan company sebab tak bagi bonus, salahkan sekolah/kolej/university sebab naikkan yuran pelajaran, salahkan hospital sebab charge hospital mahal sangat, dan bermacam-macam lagi kesalahan orang lain.

Mereka sahajalah yang tak bersalah dan menjadi mangsa keadaan.

Jadi ada antara mereka yang memberi ALASAN tak boleh nak spend untuk bersedekah, menderma, berwakaf, sebab duit utk hidup diri sendiri & family pun cukup-cukup makan aje.

Nak beli buku tambahan/tuition untuk pelajaran anak pun tak boleh. Nak hantar service maintenance kereta pun bertangguh-tangguh, sampai last-last kereta tu sendiri dah rosak teruk, dan lagi banyak nak kena repair. Semuanya sebab nak cut expenses.

Nak buat macam mana, dah rutin kerja kita PERGI PAGI, BALIK PETANG. DAPAT GAJI BAYAR HUTANG. Produktif atau tidak produktif kita di tempat kerja, akhir bulan tetap akan mendapat jumlah gaji yang sama...tetapi HUTANG & KOMITMEN semakin bertambah. Selesa sangat kah kita hidup macam tu?

Maria dulu pun sebenarnya tergolong dalam kumpulan yang suka MENGELUH ni. Tapi kini Alhamdulillah, Allah sudah sedarkan Maria tentang keburukan sifat MENGELUH ini. Kini Maria sedang berusaha untuk ke arah mencapai Financial Freedom dengan menjalankan perniagaan. Maria yakin yang 9/10 pintu rezeki adalah melalui perniagaan. Semoga Allah permudahkan.

This is a very nice article from Robert Kiyosaki, the writer of RICH DAD, POOR DAD book, on the FINANCIAL INTELLIGENCE.

Semoga ianya dapat mengubah mindset kita, supaya jangan hanya tahu BERJIMAT sahaja. Tetapi kita juga perlu tahu saluran yang terbaik untuk SPEND harta kita, agar rezeki yang Allah beri dapat DIGANDAKAN dan beri lebih manfaat kepada diri, keluarga, masyarakat dan ke arah menegakkan Islam.

ERTI HIDUP PADA MEMBERI (Pinjam ayat dari SaifulIslam.com). Selamat Membaca! :)

------------------------------------------------------------------------------------------

Don't Cut Expenses, SPEND! SPEND! SPEND! (Robert Kiyosaki)

That is LAZY advice. It’s safe advice for the so-called “advisor” because it sounds logical and it won’t cause any flack for the advisor. It’s lazy because the advisor doesn’t have to think.

Cut vs. Spend

Not only is “cut your expenses” lazy advice it is also incorrect advice if you truly want financial security for life. Consider this; you own a duplex that you rent out to two families. In any rental property, as in any business, your three key financial components are: 1) Income 2) Expenses 3) Debt. What are the first questions you should ask when it comes to income, expenses and debt?

INCOME – Very simply, “How do I increase my income?” Whether it’s your rental property, your business, or your personal household, often times, the solution to a financial problem is to increase your income. In real estate, ways to accomplish this is by lowering your vacancies, introduce alternate streams of income such as laundry, and increasing rents.

EXPENSES – Most people automatically ask, “How do I cut my expenses?” Wrong question. The better question to ask is, “How do I spend my money more effectively to increase the value of my property?” “How do I spend my money more effectively to increase the value of my business?” (And yes, this is the question to ask when it comes to you personal finances as well.)

For example, you decide the water bill of the rental duplex you own is too high so you choose to cut that expense by cutting back on the amount of water you use on the property. As a result of the water cutback, your trees and shrubs start dying. Now your tenants are unhappy because the landscape is brown and ugly.

Instead of cutting expenses, the better idea can be to spend money. As with a property I owned, instead of cutting back, I spent more money on additional trees and shrubs. This expenditure increased the curb appeal and made the property more attractive to the residents and prospective tenants.

Because this property now had such a lush look and feel, more and more people wanted to live there. This allowed me to increase the rents. Increased rents equals increased value of the property.

How do you spend money more effectively to increase the value or income, is the exact same question you should be asking of your personal finances. “How can I spend, or use, my money to make more money?”

This is what I mean when I say don’t live below your means, instead expand your means.

Instead of focusing on reducing your expenses, focus instead on INCREASING YOUR INCOME. Increasing your income - not by you working harder, but by spending money that then works hard for you. It takes no brains to cut expenses. Anyone can do that.

It takes CREATIVITY and a little bit of GUTS to figure out how to spend your money to make money. That’s FINANCIAL INTELLIGENCE.

That leaves us with the DEBT question.

The question to ask is, “How do I get the best financing terms?” Too many people focus on the price of the investment, when the deal may be found in the terms, such as the interest rate, length of the loan, interest-only versus 30-year fixed, recourse versus non-recourse. (BTW, if you don’t know the definitions of any of those words, just look them up.)

More than once, I have paid full price in exchange for terms that allowed me to get more cash flow, more time if repairs were needed, or more flexibility for future usage of the property. It’s the financing terms more than the price that can make or break a deal. The beauty of debt (good debt) today is that it is cheap. The interest rate of my first rental property in 1989 was 18%. And we still made it cash flow.

What’s the difference between good debt and bad debt?

Good debt is debt you use to buy assets with. (Assets are things that put money in your pocket whether you work or not.)

Bad debt is debt you use to buy liabilities. (Liabilities are things that take money from your pocket.)

IT’S TIME TO SPEND MONEY!

So,the real key to happiness? The key to having a secure and financially-healthy life is to Spend! Spend! Spend! Just be sure to spend your money in the right places. Financial intelligence is knowing how to spend your money to acquire assets that make money for you versus spending money to acquire liabilities that take money from you. That’s the difference that every Rich Woman knows.

How are you going to spend your money on assets?

Article taken from Richdad.com website.

COMMENTS